Market Review Q1 2023 | Market Review Q2 2023 | Market Review Q3 2023 | Market Review Q4 2023 |

Market Review Q1 2024 | Market Review Q2 2024

Third Quarter 2024

Politics Takes Second Stage

One would think that a recap of the third quarter in a historic election year would lead with the presidential race and its possible impact on the economy and financial markets. While the election does feature in the words to follow, stealing the headlines this quarter was the Federal Open Market Committee (FOMC) and their somewhat surprising announcement to cut the overnight lending rate by 50 basis points, or 0.50%, at their recent meeting in September. Following this decision there was much debate about whether the FOMC was taking too big a first step towards their ultimate goal of lower rates, but in terms of how the markets reacted, the evidence was clear... the bull market would continue.

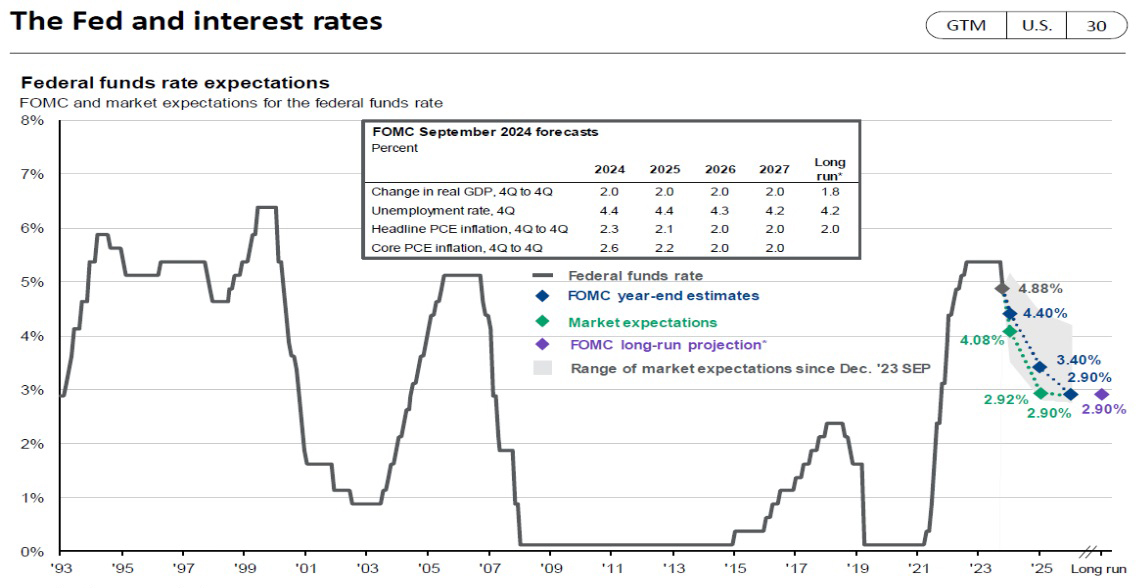

Federal Reserve - Fed Makes its Move

Coming into the September meeting of the FOMC, there was little doubt that an interest rate reduction was on the table, as Chairman Jerome Powell had made the Committee’s intentions clear coming out of August’s Jackson Hole meeting saying, “The time has come for policy to adjust.”1 The only unknown was the degree of the cut, with traders almost equally split between 0.25% and 0.50%. The Fed decided to start the reduction cycle aggressively with a 0.50% point cut – guiding from a previous range of 5.25% - 5.50% to a new targeted range of 4.50% - 5.00%. This was the first change in rates since July 2023, and notably represents the first cut since the Fed began its record expansion in rates in March 2022.

As it does after every meeting, the FOMC released its dot plot graph showing its probable path for future interest rates. The graph below shows their current thinking in blue dots overlayed against the market expectations in black dots. For the first time in quite a while, they are fairly closely aligned. Importantly, the FOMC sees 2024 ending with rates 0.50% points lower at 4.50%, and 2025 bringing rates a full point lower to 3.50%. Ultimately, the FOMC and the market see this rate cutting cycle ending with overnight rates at about 3.00% in early 2026. While this is by no means a guarantee, it does signal an expectation of significant future easing in monetary policy.

Source: Bloomberg, FactSet, Federal Reserve, J.P. Morgan Asset Management

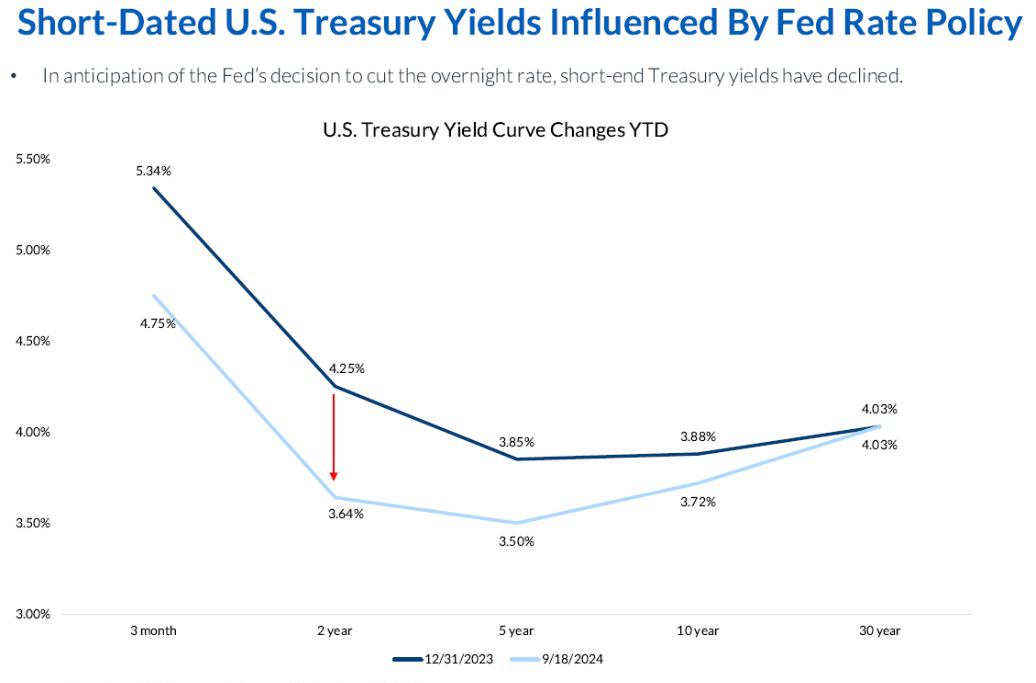

Fixed Income – Yield Curve Normalizing

As inflation continued to ease in the third quarter and the FOMC initiated a rate-cutting cycle, bonds delivered their strongest performance in a long time, with the Bloomberg Intermediate Gov/Credit index gaining 4.17%. Interest rates came down across the whole curve with the 2-year Treasury yielding 3.70% compared to 4.70% at the start of the quarter. The all-important 10-year Treasury, from which mortgage rates take their cue, fell from 4.50% to 3.80%.

The chart below shows the year-to-date changes in interest rates across the curve, with the most noticeable moves occurring in the shorter term. The 2-year Treasury is directly anchored to the likely path of the Fed and over the first nine months of 2024, this rate has dropped 61 basis points as the market now expects further interest rate cuts through 2025 and into 2026.

Source: Bloomberg U.S. Treasury Index as of September 18, 2024. Information is subject to change and is not a guarantee of future results.

Notably, during a brief stock market swoon in early August that saw the S&P 500 pull back 6% over three days, the bond market rallied strongly. Now that interest rates are noticeably higher, it appears that the recent positive correlation between stocks and bonds has ended and bonds are once again providing protection during market sell-offs.

Economy – Still Humming

The third quarter proved once again that fears of a recession were overblown as the U.S. economy continued to power forward with GDP growth expectations of 3.1%, which would be an improvement on strong second quarter growth of 3%. Long-term growth in the U.S. has been 2% so the economy is currently growing at a higher than historical rate.

There were signs of some weakening, especially from lower income consumers, who no doubt are most affected by higher price levels. However, overall consumer spending has shown few signs of abating, especially among those who own real assets and have seen their home values and portfolios at all-time high levels. Additionally, the still high interest rates on savings have helped fuel discretionary expenditures such as travel, restaurants and entertainment for those with investable savings.

The unemployment rate, though higher at 4.20%, is still within the 4.00% - 4.50% range that the FOMC considers full employment. While there are signs that the labor market is slowing, the FOMC’s current path of embarking on a rate cutting cycle will drive renewed investment and capital spending and should provide tailwinds to thwart sustained damage to the job market.

Inflation continues to normalize with the latest Personal Consumption Expenditures Price Index (PCE) coming in at 2.2%, a sharp drop from the previous month’s reading of 2.5%. We are getting closer to the FOMC’s long range target of 2.0%, and though victory over inflation can not be fully declared, we are within shouting distance.

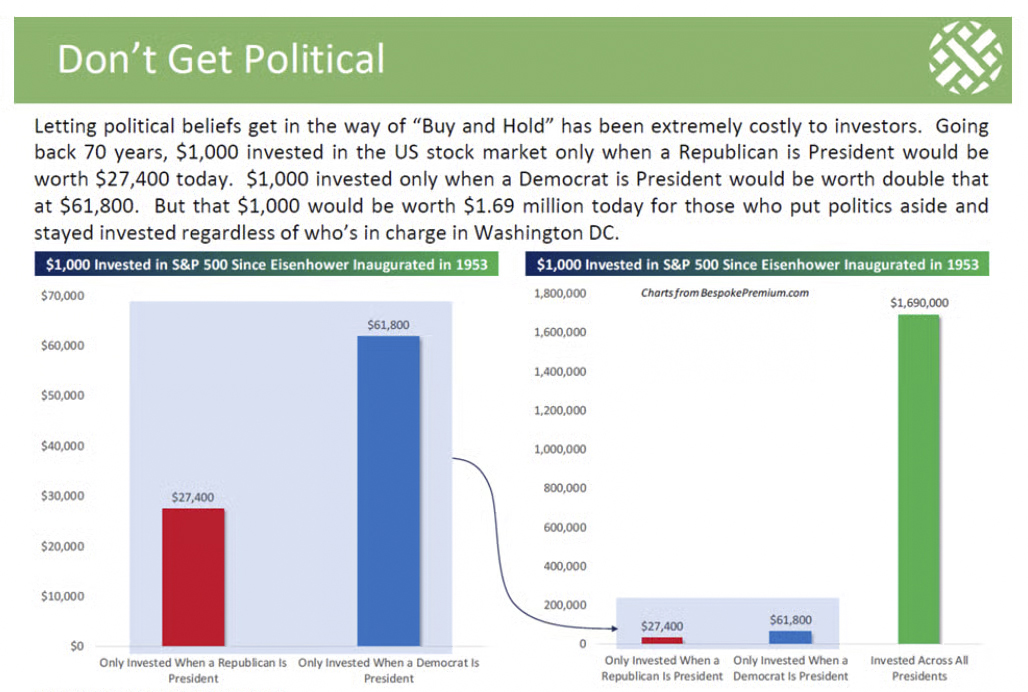

Election – Maintain Your Course

The end of the third quarter saw the upcoming election coming more into focus. There is much debate around both candidates, but what is not in question is the current level of rhetoric and polarization. The intensity of the 2024 presidential contest could easily spill over into the financial markets and lead to higher volatility. How should an investor brace for this?

We often have clients ask if they should sell out of the stock market before the election and then get back in when either their party wins or “things calm down.” The chart below shows the dangers of leaving the market to cling to the safety of your preferred party. If you had invested $1,000 in the stock market (S&P 500) and left it in only during Republican administrations, you would have $27,400 today. Conversely, leaving it invested only during Democrat regimes would give you $61,800. And if you had left that same $1,000 invested during all presidencies? You would have $1.69 million!

This is why we don’t time markets. By investing in stocks, we are showing our faith in the U.S. economy, which has continued to adapt, improve and grow – no matter who is in charge. Long term, it has made little difference to the markets who is President.

Source: Bespoke, Bloomberg. Past performance is no guarantee of future results.

Earnings – Strong group effort

Large U.S. corporations continued to show surprisingly strong earnings for the second quarter with the S&P 500 reporting earnings growth of 11.26% versus expectations of 8.69%. 2024 second half earnings are expected to slow somewhat, but overall earnings growth for the current year is expected to come in around 10%. While earnings in the technology sector showed the highest growth, double digit growth was also seen in consumer discretionary, financials, healthcare and utilities.

One factor that should be beneficial to future earnings and has helped support all-time stock market levels is the decline in interest rates. Lower rates help in two ways – companies that access the debt markets for funding should see lower interest expenses and their customers can more easily afford to finance larger purchases.

It is important to note that the market is expecting 2025 earnings growth of 15% and then further growth in 2026 of 12.5%. Current stock valuations reflect these high growth assumptions, and any shortfall could lead to stagnant or lower share prices.

Markets – Everything Working

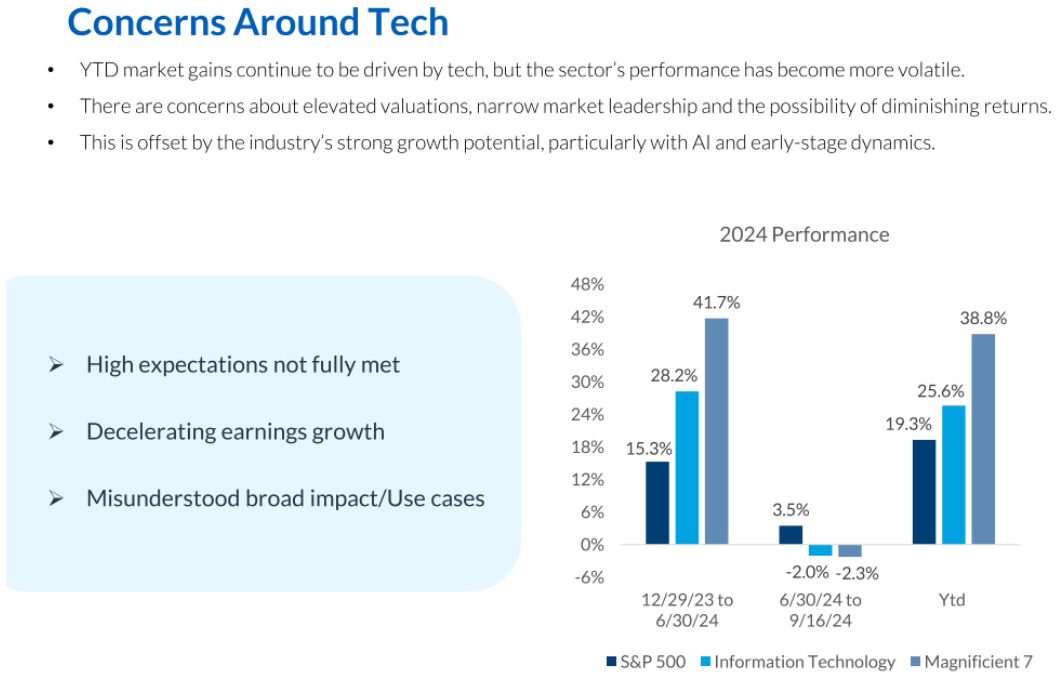

The stock market continued its torrid pace with the S&P 500 gaining 5.53% in the third quarter, which takes the year-to-date gains up to 20.81%. The best performing sectors were utilities, up 18.47%, and real estate, up 16.29%. This was not a surprise as moves in interest rates, in this case downward, have the most impact on these traditionally interest-rate-sensitive sectors. What was a surprise was the relatively weak performance in technology, which was up only 1.44% for the quarter. One marked change from the previous quarter was the strong outperformance of mid-caps, up 6.90%, and small caps, up 10.14%. Both the weakness in technology and the strong performance of smaller companies point to a healthier environment for equities, as breadth has expanded and more companies are experiencing market gains.

International equity markets were also strong, with both developed and emerging markets enjoying high single-digit returns. One laggard for the last few years that saw a surprise breakout at the end of September was China, where capital restrictions and harsh government actions towards domestic tech companies had led many investors to view the country as uninvestable. China has now joined central banks around the world by aggressively cutting their interest rates and signaling strong support for their beleaguered equity markets.

One surprise of 2024 that continued in Q3 was the price of precious metals, notably gold. The precious metals ETF we utilize for direct exposure, GLTR, was up over 24% year-to-date, exceeding even equity gains. There are many factors explaining this rise including record levels of sovereign debt that show no chance of abating, along with central banks around the world cutting interest rates, further increasing liquidity. Perhaps more importantly, gold has long been seen as a hedge against geopolitical troubles with the recent Middle East conflict spurring even further buying.

Source: Bloomberg, as of September 2024. Information is subject to change and is not a guarantee of future results.

Technology, especially related to Artificial Intelligence (AI), fueled the stock market rally through the first half of the year. This took a noticeable turn in the third quarter as shown in the chart above. The Magnificent 7, which includes Microsoft, Apple and Nvidia, surged ahead by over 40% in the first six months of 2024, but actually declined over the next ten weeks, alongside the broader technology sector. However, the S&P 500, which includes the Magnificent 7, had a positive gain for this same time period. This speaks to two factors – investors finally containing their excitement over AI until they see evidence of product-related growth and a healthy broadening of the bull market we’ve been in this year as investors find other non-technology companies to purchase.

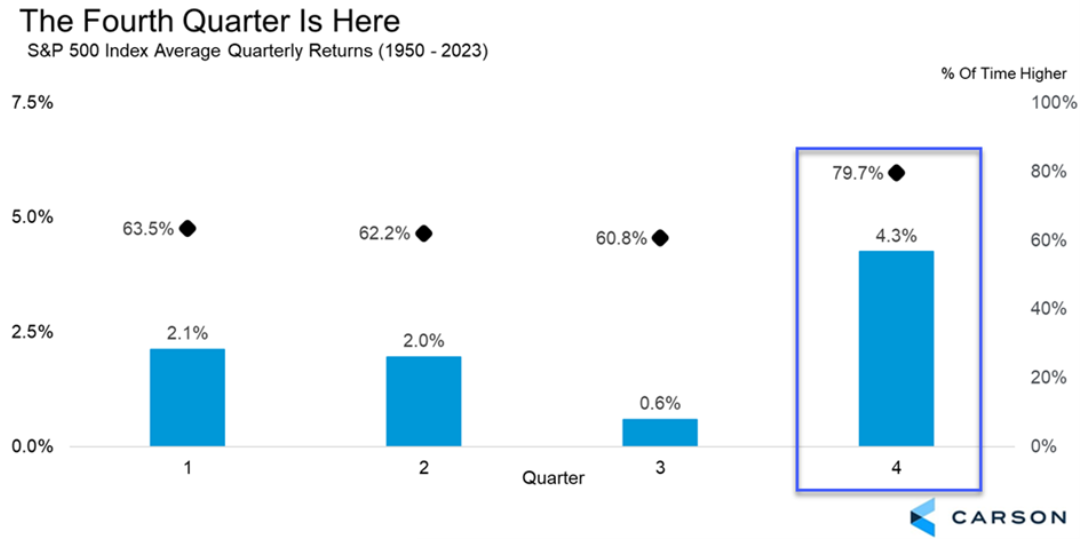

Final Lap of 2024 – Remain Seated

As we enter the fourth quarter and the usual volatile month of October, many investors will be tempted to sit out investing in the stock market completely, especially in a year that features a hotly contested presidential election. However, historically, this is the best quarter to be in the stock market as seen in the chart below. This is not the time to doubt your long-term confidence in the U.S. economy and its capital markets.

Source: Carson Investment Research, YCharts 09/28/2024

We at Cape Cod 5 know that the domestic backdrop for investing may have become more unnerving as a polarizing election and growing geopolitical conflict add to the usual litany of worries. Ultimately, portfolios will likely be heavily influenced by the FOMC moves and rate environment. As always, we will be here monitoring economic developments, including any potential impacts from the election, and new market information to ensure your portfolios are best positioned for the path ahead.

We appreciate your confidence in our financial stewardship and are always here to speak with you.

Jonathan J. Kelly, CFP®, CPA

Senior Investment Officer

On behalf of the Cape Cod 5 Trust and Asset Management Investment Team

Michael S. Kiceluk, CFA, Chief Investment Officer

Brad C. Francis, CFA, Director of Research

Rachael Aiken, CFP®, Senior Investment Officer

Jonathan J. Kelly, CFP®, CPA, Senior Investment Officer

Nancy Taylor, CFA, CAIA®, Senior Investment Officer

Robert D. Umbro, Senior Investment Officer

Benjamin M. Wigren, Senior Investment Officer

Kimberly K. Williams, Senior Wealth Management Officer

Craig J. Oliveira, CFA, Investment Officer

Jack Dailey, Investment Analyst

Alecia N. Wright, Investment Analyst

1 Barron's, https://www.barrons.com/livecoverage/jackson-hole-fed-meeting-powell-speech

These facts and opinions are provided by the Cape Cod 5 Trust and Asset Management Department. The information presented has been compiled from sources believed to be reliable and accurate, but we do not warrant its accuracy or completeness and will not be liable for any loss or damage caused by reliance thereon. Investments are NOT A DEPOSIT, NOT FDIC INSURED, NOT INSURED BY ANY FEDERAL GOVERNMENT AGENCY, NOT GUARANTEED BY THE FINANCIAL INSTITUTION AND MAY GO DOWN IN VALUE.